That “cheap” used car might be the most expensive vehicle you ever buy.

The real cost of owning a used car goes far beyond the sticker price, loan payment, or the cash you hand over on purchase day. Repairs, insurance, fuel, taxes, depreciation, and missed maintenance can quietly turn a bargain into a budget drain.

Before you fall for a low asking price, you need to estimate what the car will actually cost to own month after month. That means looking at its age, mileage, reliability history, service records, and the common failures that come with that specific model.

This guide will show you how to calculate the true cost of a used car so you can compare options clearly, avoid financial surprises, and buy with confidence instead of hope.

What “Total Cost of Ownership” Means for a Used Car

Total cost of ownership is the real amount you spend to buy, drive, maintain, insure, and eventually sell a used car. The purchase price is only one part of the equation, and it can be misleading if you ignore car insurance rates, auto loan interest, fuel economy, repair costs, registration fees, and depreciation.

For example, a used BMW may cost the same upfront as a used Toyota Camry, but the BMW could require higher insurance premiums, premium fuel, expensive tires, and more costly repairs. In real-world ownership, I’ve seen “cheap” luxury cars become expensive quickly because routine maintenance and parts pricing were never factored in before purchase.

A practical total ownership estimate should include:

- Financing costs: monthly payment, loan term, APR, and lender fees.

- Operating costs: fuel, oil changes, tires, brakes, and scheduled maintenance.

- Risk costs: insurance, unexpected repairs, warranty coverage, and resale value.

Before buying, use tools like Kelley Blue Book, Edmunds, or RepairPal to compare resale value, common repair costs, and fair market pricing. Also request insurance quotes before signing, because the same driver may pay very different rates depending on the vehicle’s safety rating, theft risk, engine size, and repair history.

The goal is simple: compare cars based on what they will cost over time, not just what the seller is asking today. That shift can prevent an affordable-looking used car from becoming a monthly budget problem.

How to Calculate Used Car Ownership Costs Before You Buy

Start by looking beyond the sticker price and building a monthly ownership estimate before you make an offer. A reliable used car cost calculator, such as Kelley Blue Book or Edmunds True Cost to Own, can help you compare depreciation, insurance rates, fuel economy, maintenance, repairs, registration fees, and financing costs in one place.

For a practical estimate, collect the car’s VIN, mileage, trim level, and your ZIP code. Those details matter because auto insurance quotes, sales tax, vehicle registration fees, and even repair labor rates can change significantly by location.

- Loan payment: Use an auto loan calculator with the actual APR, down payment, and loan term.

- Insurance cost: Get quotes before buying, especially for SUVs, luxury cars, or salvage-title vehicles.

- Maintenance and repairs: Check common problems through owner forums, service records, and a pre-purchase inspection.

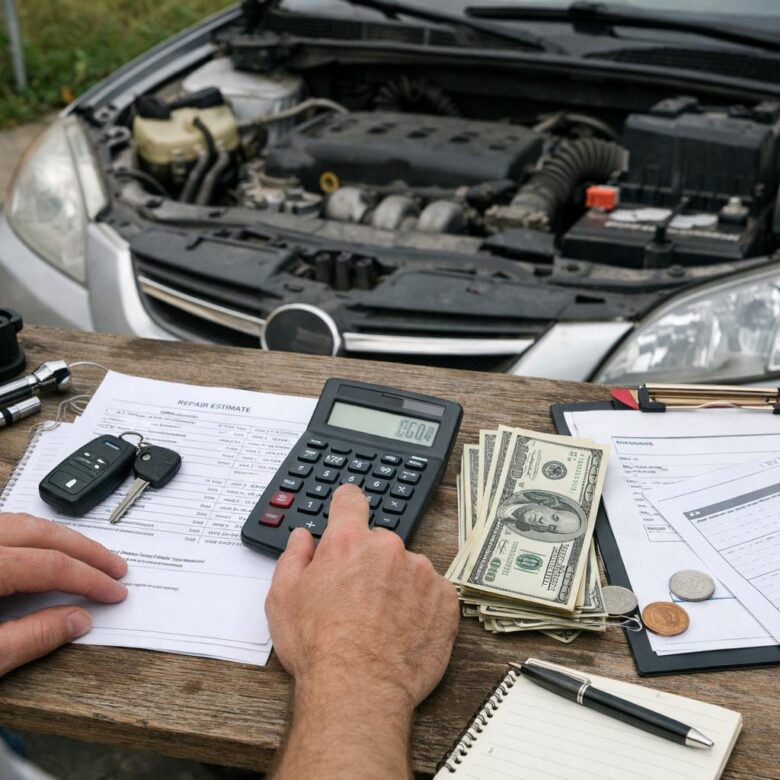

For example, a $14,000 used sedan may look cheaper than a $17,000 hybrid, but the sedan could cost more over time if it has higher fuel costs, expensive tires, and a timing belt service due soon. I’ve seen buyers negotiate hard on price, then get surprised by a $1,200 repair within the first month because they skipped the inspection.

A good rule is to calculate the total monthly cost, not just the car payment. Add fuel, insurance, maintenance savings, parking, tolls, and expected repairs, then compare that number with your budget before signing anything.

Common Costly Mistakes That Make a Used Car More Expensive

One of the most expensive mistakes is focusing only on the purchase price and ignoring ownership costs. A used luxury SUV with a tempting low price can still require premium tires, higher insurance premiums, expensive brake service, and specialized repairs that quickly erase any “deal.”

Skipping a pre-purchase inspection is another costly shortcut. A $150-$250 inspection by a trusted mechanic can reveal oil leaks, worn suspension parts, accident damage, or transmission issues before you sign the paperwork.

- Not checking a vehicle history report through Carfax or AutoCheck.

- Accepting the first auto loan offer without comparing interest rates.

- Buying without getting insurance quotes first.

I’ve seen buyers choose a cheaper car with a bad maintenance history, then spend more in the first six months than they saved upfront. For example, a used sedan priced $1,500 below market value may still be a poor buy if it needs tires, timing belt service, and an air conditioning repair right away.

Another overlooked mistake is ignoring fuel economy and registration fees. A larger engine, poor MPG rating, or higher local taxes can quietly increase your monthly car ownership cost, especially if you commute daily.

Before buying, compare estimated repair costs on RepairPal, check fair market value on Kelley Blue Book, and request insurance quotes from at least two providers. These small steps help you avoid hidden costs and make a smarter decision before the car becomes your financial problem.

Key Takeaways & Next Steps

The real cost of a used car is rarely the price on the windshield. A smart purchase starts with knowing what the vehicle will likely demand from your budget after you drive it home.

Practical rule: buy the car that fits both your upfront budget and your ongoing comfort level for repairs, insurance, fuel, taxes, and depreciation.

- Walk away if the numbers rely on luck or unusually low repair costs.

- Choose the car with the most predictable ownership costs, not just the lowest price.

A used car is a good deal only when it remains affordable over time.

Dr. Marcus Ellington is an automotive education specialist with a background in consumer mobility, vehicle ownership guidance, and practical driving safety. He writes clear, reliable car guides to help everyday drivers make smarter decisions about maintenance, ownership costs, insurance, and road readiness.